Analyse PLS-SEM

Comprendre, exécuter et interpréter votre modèle d’équations structurelles par moindres carrés partiels.

Qu’est-ce que le PLS-SEM ?

Le PLS-SEM (Partial Least Squares – Structural Equation Modeling), ou « modèle d’équations structurelles par moindres carrés partiels », est une méthode statistique qui permet de tester simultanément des liens de cause à effet entre des concepts abstraits — appelés variables latentes — qui ne peuvent pas se mesurer directement.

Vous ne pouvez pas mesurer la « Confiance » d’un client avec un thermomètre. En revanche, vous pouvez poser 4 ou 5 questions sur une échelle de 1 à 7 :

« Cette technologie me semble fiable », « Je ferais confiance à ses recommandations »…

Le PLS transforme ces réponses en un score synthétique (« variable latente »), puis teste si ce score influence d’autres concepts comme l’Intention d’utilisation. C’est ça, un modèle PLS : des flèches de causalité entre des concepts abstraits, tous construits à partir de vos questions de terrain.

Comment ça fonctionne, étape par étape

Les 4 critères-clés que le code calcule pour vous

Alpha de Cronbach

Mesure si les questions d’un même bloc sont cohérentes entre elles. Si le score est faible, vos répondants n’ont pas compris les questions de la même façon.

Seuil ≥ 0,70AVE

Average Variance Extracted : vérifie que vos questions capturent bien le concept qu’elles sont censées mesurer, et non du bruit aléatoire.

Seuil ≥ 0,50VIF

Variance Inflation Factor : s’assure que deux variables ne font pas « double emploi ». Un VIF élevé rend les coefficients instables et peu fiables.

Seuil < 5,00Matrice HTMT

Test le plus sévère : prouve que deux concepts sont bien distincts dans l’esprit du répondant. Si le score est trop proche de 1, les concepts se confondent.

Seuil < 0,85 – 0,90Avant de lancer le code : étape cruciale

Le script Python lit vos données depuis un fichier Excel. Vous devez impérativement modifier le nom du fichier à la ligne 10 du code selon votre groupe :

| Votre groupe | Nom du fichier à inscrire dans le code |

|---|---|

| L3 MRC et IHR | BASE-MRC-IHR.xlsx |

| L3 MHR Hébergement | BASE-Hbgt.xlsx |

| L3 MHR Restauration | BASE-MHR-Rest.xlsx |

Attention : Si le nom ne correspond pas exactement (majuscules, tirets, extension…), le programme affichera une erreur “File Not Found” et ne pourra pas démarrer.

Téléchargement des bases de données

Téléchargez le fichier Excel correspondant à votre groupe et importez-le dans votre session Google Colab :

Le code Python (Version Expert)

Ce code calcule automatiquement les Coefficients, le Bootstrap, le VIF, l’AVE et la matrice HTMT. Copiez ce script dans Google Colab :

import pandas as pd

import numpy as np

from sklearn.model_selection import cross_val_predict

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error, r2_score

import statsmodels.api as sm

from statsmodels.stats.outliers_influence import variance_inflation_factor

from tqdm import tqdm

# ==========================================

# === 1) CONFIGURATION ET LECTURE DU FICHIER

# ==========================================

FILE_PATH = "/content/BASE-MRC-IHR.xlsx"

SHEET_NAME = "BASE"

df = pd.read_excel(FILE_PATH, sheet_name=SHEET_NAME)

print(f"Fichier chargé : {FILE_PATH} | Taille : {df.shape}")

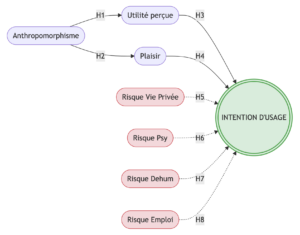

# Blocs de mesure — construits impliqués dans H1–H6 + H_Dehum + H_Emploi

blocks = {

"Anthropomorphisme": ["ANT1","ANT2","ANT3","ANT4","ANT5"],

"Utilite": ["UTIL1","UTIL2","UTIL3","UTIL4","UTIL5","UTIL6","UTIL7"],

"Plaisir": ["PLAIS1","PLAIS2","PLAIS3","PLAIS4"],

"RisqueViePrivée": ["RCONTETH1","RCONTETH2","RCONTETH3","RCONTETH4"],

"RisquePsy": ["RPSY1","RPSY2","RPSY3"],

"RisqueDehum": ["RDEHUM1","RDEHUM2","RDEHUM3","RDEHUM4","RDEHUM5"], # NOUVEAU

"RisqueEmploi": ["RPEMP1","RPEMP2","RPEMP3","RPEMP4","RPEMP5"], # NOUVEAU

"Intention": ["INT1","INT2","INT3","INT4"]

}

# Topographie du réseau (Inner Model)

# Ajout de RisqueDehum → Intention et RisqueEmploi → Intention

base_relations = [

("Anthropomorphisme", "Utilite"), # H1

("Anthropomorphisme", "Plaisir"), # H2

("Plaisir", "Intention"), # H3

("Utilite", "Intention"), # H4

("RisqueViePrivée", "Intention"), # H5

("RisquePsy", "Intention"), # H6

("RisqueDehum", "Intention"), # H_Dehum — NOUVEAU

("RisqueEmploi", "Intention") # H_Emploi — NOUVEAU

]

# Modèle Structurel (Équations)

# Intention intègre désormais les deux nouveaux prédicteurs de risque

equations = {

"Utilite": ["Anthropomorphisme"], # H1

"Plaisir": ["Anthropomorphisme"], # H2

"Intention": ["Plaisir", "Utilite", "RisqueViePrivée", "RisquePsy",

"RisqueDehum", "RisqueEmploi"] # H3–H6 + Dehum + Emploi

}

all_items = [item for sublist in blocks.values() for item in sublist]

df_items = df[all_items].dropna().copy()

# ==========================================

# === 2) L'ALGORITHME ITERATIF PLS-SEM

# ==========================================

def run_pls_sem(data_raw, blks, relations, max_iter=100, tol=1e-5):

X = (data_raw - data_raw.mean()) / data_raw.std()

lv_names = list(blks.keys())

C = pd.DataFrame(0.0, index=lv_names, columns=lv_names)

for s, t in relations:

if s in lv_names and t in lv_names:

C.loc[s, t] = 1.0

C.loc[t, s] = 1.0

Y = pd.DataFrame({lv: X[items[0]] for lv, items in blks.items()})

for _ in range(max_iter):

Y_old = Y.copy()

E = Y.corr() * C

Z = Y.dot(E)

Z = (Z - Z.mean()) / Z.std()

W = {}

for lv, items in blks.items():

w = X[items].apply(lambda col: col.cov(Z[lv]))

w = w / np.linalg.norm(w)

W[lv] = w

Y[lv] = X[items].dot(w)

Y = (Y - Y.mean()) / Y.std()

if np.abs(Y - Y_old).max().max() < tol:

break

Loadings = {lv: X[items].apply(lambda col: col.corr(Y[lv])) for lv, items in blks.items()}

return Y, W, Loadings

Y_final, W_final, L_final = run_pls_sem(df_items, blocks, base_relations)

# La fonction est conservée mais ne crée plus de variables d'interaction

def calculate_inner_variables(Y_df):

return Y_df.copy()

Y_complet = calculate_inner_variables(Y_final)

# ==========================================

# === 3) CALCUL DES CRITÈRES DE QUALITÉ

# ==========================================

qualite_list = []

loadings_df_list = []

for lv, loadings in L_final.items():

for item, l_val in loadings.items():

loadings_df_list.append({"Construit": lv, "Item": item, "Loading_Wold": l_val})

n = len(blocks[lv])

corr_matrix = df_items[blocks[lv]].corr()

avg_corr = corr_matrix.values[np.triu_indices(n, k=1)].mean() if n > 1 else 1.0

alpha = (n * avg_corr) / (1 + (n - 1) * avg_corr) if n > 1 else 1.0

ave = np.mean(loadings**2)

sum_l = np.sum(loadings)

sum_e = np.sum(1 - loadings**2)

cr = (sum_l**2) / (sum_l**2 + sum_e)

qualite_list.append({"Variable": lv, "Cronbach_Alpha": alpha, "Composite_Reliability": cr, "AVE": ave})

df_loadings = pd.DataFrame(loadings_df_list)

df_qualite = pd.DataFrame(qualite_list)

X_std = (df_items - df_items.mean()) / df_items.std()

latent_names = list(blocks.keys())

htmt_df = pd.DataFrame(index=latent_names, columns=latent_names, dtype=float)

for i, b1 in enumerate(latent_names):

for j, b2 in enumerate(latent_names):

if i == j:

htmt_df.iloc[i,j] = 1.0

elif i < j:

items1, items2 = blocks[b1], blocks[b2]

hetero_mean = X_std[items1 + items2].corr().loc[items1, items2].values.mean()

mono1 = X_std[items1].corr().values[np.triu_indices(len(items1), k=1)].mean() if len(items1)>1 else 1.0

mono2 = X_std[items2].corr().values[np.triu_indices(len(items2), k=1)].mean() if len(items2)>1 else 1.0

htmt_val = abs(hetero_mean / np.sqrt(max(0.0001, abs(mono1 * mono2))))

htmt_df.iloc[i,j] = htmt_val

htmt_df.iloc[j,i] = htmt_val

fl_matrix = Y_final.corr()

for b in latent_names:

fl_matrix.loc[b, b] = np.sqrt(df_qualite.loc[df_qualite['Variable'] == b, 'AVE'].values[0])

# ==========================================

# === 4) MODELE STRUCTUREL (R², f², VIF)

# ==========================================

results_inner = {y: sm.OLS(Y_complet[y], sm.add_constant(Y_complet[xs])).fit() for y, xs in equations.items()}

structurel_data = []

for dep, preds in equations.items():

X_mat = sm.add_constant(Y_complet[preds])

R2_incl = results_inner[dep].rsquared

for i, p in enumerate(preds, start=1):

vif = variance_inflation_factor(X_mat.values, i)

preds_excl = [x for x in preds if x != p]

R2_excl = 0 if not preds_excl else sm.OLS(Y_complet[dep], sm.add_constant(Y_complet[preds_excl])).fit().rsquared

f2 = (R2_incl - R2_excl) / (1 - R2_incl)

structurel_data.append({

"Variable_Dep": dep, "Predictor": p,

"Coefficient": results_inner[dep].params[p],

"f2": f2, "VIF": vif

})

df_structurel = pd.DataFrame(structurel_data)

# ==========================================

# === 5) BOOTSTRAPPING (t-values)

# ==========================================

def run_bootstrap(data_raw, n_boot=500):

rng = np.random.default_rng(123)

boot_coefs = []

for _ in tqdm(range(n_boot), desc="Bootstrapping PLS"):

sample = data_raw.sample(len(data_raw), replace=True, random_state=rng.integers(0, 100000))

Y_boot, _, _ = run_pls_sem(sample, blocks, base_relations, max_iter=30)

Y_boot_comp = calculate_inner_variables(Y_boot)

row = {}

for dep, preds in equations.items():

res = sm.OLS(Y_boot_comp[dep], sm.add_constant(Y_boot_comp[preds])).fit()

for p in preds:

row[(dep, p)] = res.params[p]

boot_coefs.append(row)

return pd.DataFrame(boot_coefs)

boot_df = run_bootstrap(df_items, n_boot=500)

boot_std = boot_df.std()

boot_ci = boot_df.quantile([0.025, 0.975]).T

boot_ci.columns = ["CI_lower", "CI_upper"]

df_structurel["t-value"] = df_structurel.apply(

lambda r: abs(r["Coefficient"] / boot_std[(r["Variable_Dep"], r["Predictor"])]), axis=1

)

df_structurel["p-value"] = [results_inner[r["Variable_Dep"]].pvalues[r["Predictor"]] for _, r in df_structurel.iterrows()]

df_structurel["Significatif_t"] = df_structurel["t-value"] > 1.96

# ==========================================

# === 6) FIT GLOBAL (SRMR) & MACHINE LEARNING (Q² / PLSpredict)

# ==========================================

# --- SRMR ---

R_obs = df_items.corr()

R_implied = pd.DataFrame(np.eye(len(all_items)), index=all_items, columns=all_items)

lv_corr = Y_complet[latent_names].corr()

item_lv_map = {item: lv for lv, items in blocks.items() for item in items}

item_loading_map = {item: L_final[lv][item] for lv, items in blocks.items() for item in items}

for i in range(len(all_items)):

for j in range(i+1, len(all_items)):

it1, it2 = all_items[i], all_items[j]

lv1, lv2 = item_lv_map[it1], item_lv_map[it2]

r_imp = item_loading_map[it1] * item_loading_map[it2] * lv_corr.loc[lv1, lv2]

R_implied.loc[it1, it2] = r_imp

R_implied.loc[it2, it1] = r_imp

diff = R_obs.values - R_implied.values

mask = np.triu(np.ones(diff.shape), k=1).astype(bool)

srmr_value = np.sqrt(np.mean(diff[mask]**2))

df_srmr = pd.DataFrame([{

"Metric": "SRMR Global", "Valeur": srmr_value,

"Seuil": "< 0.08 (Idéal) / < 0.10 (Acceptable)",

"Statut": "Excellent" if srmr_value < 0.08 else ("Acceptable" if srmr_value < 0.10 else "À revoir")

}])

# --- Q² (10-Fold CV sur modèle structurel) ---

lr = LinearRegression()

q2_list = []

for dep, preds in equations.items():

y_pred_cv = cross_val_predict(lr, Y_complet[preds], Y_complet[dep], cv=10)

q2_list.append({

"Variable Endogène": dep,

"R2_In_Sample": results_inner[dep].rsquared,

"Q2_Predictive_Relevance": r2_score(Y_complet[dep], y_pred_cv)

})

df_q2 = pd.DataFrame(q2_list)

# --- PLSpredict (Items endogènes - Uniquement sur l'Intention) ---

plspredict_list = []

endog_targets = ["Intention"]

for target_lv in endog_targets:

for item in blocks[target_lv]:

y_item = df_items[item]

exog_lvs = equations[target_lv]

exog_items = list(set([it for ex in exog_lvs if ex in blocks for it in blocks[ex]]))

X_item_lm = df_items[exog_items] if exog_items else df_items.drop(columns=[item])

y_pred_lm = cross_val_predict(lr, X_item_lm, y_item, cv=10)

y_pred_naive = np.full_like(y_item, y_item.mean())

rmse_lm = np.sqrt(mean_squared_error(y_item, y_pred_lm))

rmse_naive = np.sqrt(mean_squared_error(y_item, y_pred_naive))

q2_predict_item = 1 - (mean_squared_error(y_item, y_pred_lm) / mean_squared_error(y_item, y_pred_naive))

plspredict_list.append({

"Cible": target_lv, "Indicateur": item,

"RMSE_Machine_Learning (LM)": rmse_lm, "RMSE_Moyenne_Naive": rmse_naive,

"Q2_predict": q2_predict_item,

"Pouvoir_Predictif": "Fort" if rmse_lm < rmse_naive else "Faible"

})

df_plspredict = pd.DataFrame(plspredict_list)

# ==========================================

# === 7) EXPORT EXCEL EXHAUSTIF

# ==========================================

filename = "Resultats_Analyse_Expert_PLS.xlsx"

with pd.ExcelWriter(filename) as writer:

df_structurel.to_excel(writer, sheet_name='Paths_tvalue_f2_VIF', index=False)

df_srmr.to_excel(writer, sheet_name='Fit_SRMR', index=False)

df_q2.to_excel(writer, sheet_name='Q2_Relevance_Structurelle', index=False)

df_plspredict.to_excel(writer, sheet_name='PLSpredict_Items', index=False)

df_loadings.to_excel(writer, sheet_name='Loadings_Items', index=False)

df_qualite.to_excel(writer, sheet_name='Fiabilite_Mesure', index=False)

fl_matrix.to_excel(writer, sheet_name='Fornell_Larcker')

htmt_df.to_excel(writer, sheet_name='Validite_HTMT')

print(f"Modèle étendu exécuté avec succès. Fichier généré : {filename}")

Comment lire votre fichier Excel ?

Le fichier « Resultats_Analyse_Expert_PLS.xlsx » contient plusieurs onglets. Voici comment interpréter chacun d'eux :

Pour valider vos hypothèses. Si la colonne « Significatif » affiche True, l'impact causal est réel et statistiquement prouvé.

Vérifiez que l'AVE > 0,50 et l'Alpha de Cronbach > 0,70 pour chaque variable latente.

Tous les VIF doivent être inférieurs à 5. Au-delà, les résultats sont instables et peu interprétables.

Chaque score doit être < 0,85 ou 0,90 pour prouver que vos concepts sont bien distincts les uns des autres.

Indique la part de variance expliquée par votre modèle. Plus proche de 1, plus votre modèle est puissant.

Mesure la pertinence prédictive : votre modèle fait-il mieux que de simplement prédire la moyenne ?

Accès aux résultats par groupe

Sélectionnez votre groupe ci-dessous pour accéder directement à la page de consultation de vos résultats :